![]()

#

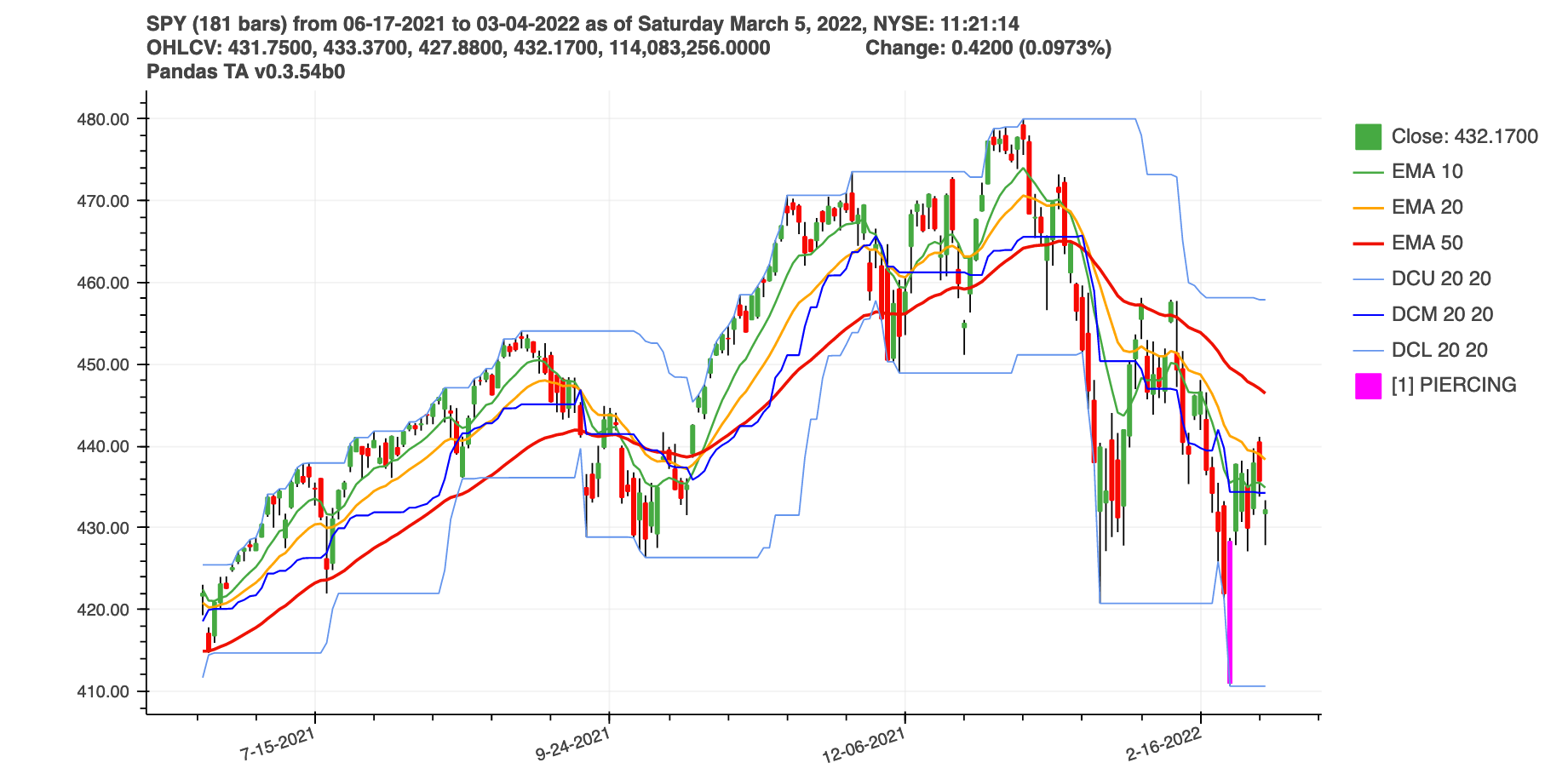

A Popular and comprehensive Technical Analysis Library in Python 3 that leverages numba and numpy for accuracy and performance, and pandas for simplicity and bulk processing. The library contains more than 150 indicators and utilities and more than 60 Candlestick Patterns (when TA Lib is installed).

It's simplicty and seamless integration makes it ideal for both novices and experienced developers building market analysis workflows and trading systems. Users include international traders, investors, quants, algorithmic trading platforms, Data Science practioners, and financial funds.

![]()

![]()

NOTICE

Thanks to all those that have sponsored and dontated to the library

in the past! Your support has been greatly appreciated!

However, future releases are on definite hold until 100+ donations of $150+ have been received via Buy Me a Coffee.

Help keep this library and application the best in it's class!

Features#

-

Easy to Use

- Conventional calling similar to TA Lib.

- Simplified usage with the Pandas DataFrame Extension "ta".

- Data Source and post analytics agnostic.

-

Large Library

- Flat library structure.

- Has 150+ indicators without TA Lib.

- Candlestick indicators with TA Lib.

- Custom Directory Support

-

Accurate & Performant

- Numpy and Numba benefits.

- Highly correlated with TA Lib and sometimes Trading View.

-

Library Status

- Your support is vital to its future!

- Maintaining this library requires ongoing support through contributions, donations & sponsorship.

- ☠️ Current levels are unsustainable and risks discontinuation.

Help

With so many indicators, it can be difficult to keep track of all the

different indicator arguments. For more details about an indicator,

run help(ta.indicator_name), e.g. help(ta.macd) or see the

API section.